We all know a big trend in the financial advisory world today is moving upmarket and serving increasingly wealthy clients. Chances are, that’s one of your key goals if you’re reading this.

But when it comes to moving really upmarket and serving the ultra-wealthy—clients with $25 million or more of net worth excluding their personal residence—advisors tend to get a little nervous. They think they don’t have what it takes to effectively work with this rarified group.

I think those advisors are wrong, and that most of them can climb the wealth ladder and effectively attract, serve and retain the ultra-wealthy. Yes, it requires a concerted effort—but it can take far less time than you might think, if you know what you’re doing.

What The Ultra-Wealthy Want

CEG Insights’ research into the ultra-wealthy reveals their key concerns and expectations when it comes to working with financial advisors. Consider just a few of the findings:

1. The ultra-wealthy want to collaborate with you. These clients aren’t going to fully delegate wealth management decisions to you. Overall, 82.1% want to be actively involved in day-to-day investment management. Among ultra-wealthy millennials—who make up more than 40% of this cohort, by the way—this desire is nearly universal (94.8%). What’s more, 79% of ultra-wealthy investors overall say that they enjoy investing and do not want to give it up. To serve the ultra-wealthy, you need to be prepared to work with them and solicit their opinions, not simply tell them what to do based on your views.

2. They want their financial lives coordinated. Given their sizable net worth, it’s not surprising that ultra-wealthy investors work with a diverse range of professional advisors—most commonly accountants, RIAs, full-service brokers, attorneys and others. The use of multiple advisors obviously dilutes the proportion of assets with any one firm. Example: Ultra-wealthy investors working with a single advisor place an average of 85% of their assets with that advisor; they manage the remaining assets themselves. When investors work with two firms, however, the primary firm manages an average of 65.6% of their assets and the secondary firm one quarter of the assets.

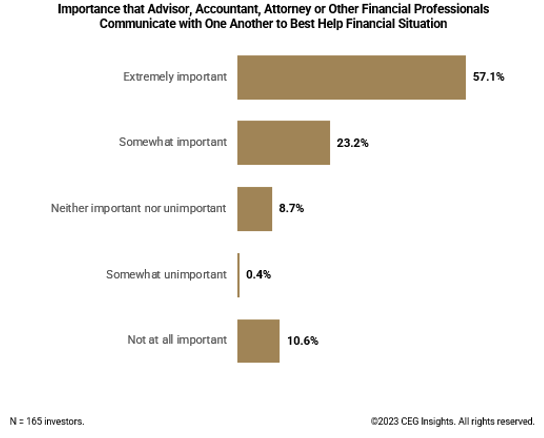

Despite the “advisor diversification,” our research indicates that the ultra-wealthy want their financial lives coordinated. Four out of five (80.3%) believe that it is either extremely or somewhat important for their advisor, accountant, attorney and other financial professionals to communicate with one another about optimizing their financial situation (see the chart).

3. They are worried about their heirs. Ultra-wealthy investors indicate that they intend to leave 56.4% of assets to children and grandchildren upon death. But even though our survey respondents on average are leaving more than half of their assets to kids or grandkids, most—77.5%—are worried that the next generation may waste that money.

Legacy planning services therefore represent a major way to attract and serve the ultra-wealthy. When you build relationships with the next generation, you increase the likelihood that they will continue to use your services after inheriting their parents’ wealth. This helps ensure the continuation of a wealthy client base, providing long-term stability and growth to your practice. It also can create opportunities for offering additional services tailored to the different needs of younger clients. And when you serve multiple generations of a family, you position yourself as a trusted family advisor, leading to increased loyalty and yet deeper client relationships.

In short, when it comes to both retaining wealthy clients and serving them extremely well, engaging members of the younger generations may be among the most powerful strategies available to you.

Action Steps

Based on the empirical research, there are several action steps that can help you attract and retain ultra-wealthy clients and, in doing so, significantly accelerate your organic growth.

1. Embrace active client involvement. Adopt a collaborative approach to investment management, particularly with younger clients. This means that while you can present options and recommendations, you should make decisions jointly with clients. Advisors who treat their clients like partners in decision-making will develop stronger, more loyal client relationships.

2. Go beyond investment management. Since no one person can be an expert in providing the myriad services the ultra-wealthy want and expect, work with your in-house experts or, if these are not available to you, create a network of professional advisors who together can meet the entire range of ultra-wealthy needs.

3. Create a virtual family office. By coordinating a virtual network of specialists, you can emulate the expertise of traditional family offices. This approach positions you attractively for the ultra-wealthy, especially those in the $25 million+ category, aligning your practice with their sophisticated needs and enhancing your appeal among the affluent market.

4. Open the door to the next generation. Foster relationships with clients’ children and grandchildren by engaging them in conversations about issues that matter to multiple generations, such as efficient wealth transfer, philanthropic goals and business succession. For example, you might build these relationships while fostering family cohesion through the use of well-organized and facilitated family meetings.

Ultimately, by understanding what the ultra-affluent want and need, and then taking informed action, you’ll position yourself to play to win by fine-tuning the direction of your practice, initiating innovative endeavors and setting yourself apart from competitors—all while bolstering your organic growth rate.

John J. Bowen Jr. is the CEO and founder of CEG Worldwide and CEG Insights. Ready to race up the hierarchy of advisor success by attracting more affluent clients to your doorstep? Schedule your Play to Win consultation today to see how CEG Worldwide can help you accelerate your success and take your practice to the next level.