In today’s article, we examine the real estate sector, specifically commercial real estate, analyze the performance and valuations for the different industries within the sector, and assess their prospects.

What Is Commercial Real Estate?

Real estate can be divided into two segments: residential and commercial. Residential real estate is largely comprised of single-family homes and condominiums, while commercial real estate is comprised of properties purchased for business use, such as: office, retail, industrial and multi-family housing.

State Of The Commercial Real Estate Sector

Commercial real estate (CRE) has been under immense pressure since the onset of Covid-19, as restrictive lockdown policies forced employees to work from home and consumers to shop online, leading to significant vacancies across office and retail properties. Additionally, restrictive monetary policy and elevated inflation have led to a meaningful increase in mortgage payments, sending interest as a percentage of loan balances dramatically higher and leading some tenants to default on their payments. However, the same headwinds that office and retail real estate have faced—a shift to remote work and digital shopping—have been tailwinds for industrial and data center real estate.

Regional banks, which suffered significant losses in early 2023 due to unrealized losses on securities and loan portfolios as interest rates rose, continue to be under scrutiny as they have relatively large exposure to CRE loans. With interest rates expected to be higher for longer, employers shifting to more flexible work-from-home policies, and e-commerce activity increasing, delinquencies are expected to continue.

Performance And Valuation

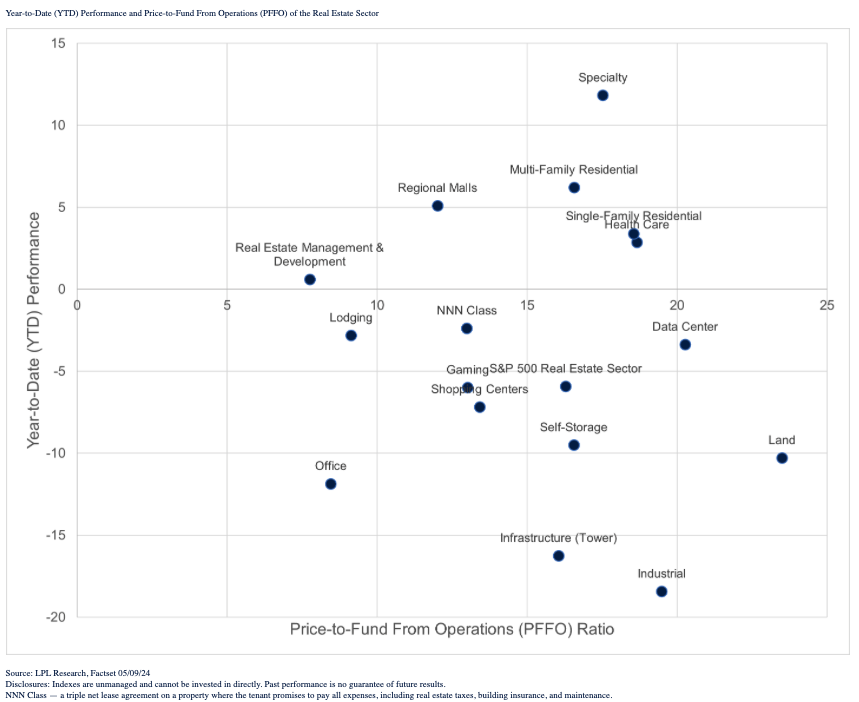

Given the headwinds in real estate, it’s no surprise the sector is the worst performer over the year-to-date period—the only sector in negative territory. The lackluster performance has positioned the real estate sector as the smallest sector component within the S&P 500. When looking at sub-sectors within real estate, you notice performance (y-axis) has varied meaningfully year to date.

Office REITs Continue To Lag Sector Peers

As highlighted above, specialty real estate investment trusts (REITs) are the top-performing sub-sector within real estate, while industrial REITs are the worst-performing sub-sector. From a valuation perspective, it seems land REITs are the most expensive, with a PFFO ratio of 23.5. This compares to the S&P 500 real estate sector average of 16.3. The cheapest sub-sector of real estate appears to be real estate management and development with a PFFO of 7.8.

As mentioned earlier, the transition to a more flexible remote working policy has hurt office REITs, with performance down over double-digits year to date. Despite the poor performance, office REITs trade at a relative discount to the real estate sector broadly, and to sub-sectors that have benefitted from the shift to digital, including data center REITs. You’ll notice infrastructure (tower) and industrial REITs have also suffered significant losses this year, despite being benefactors of artificial intelligence (AI) (infrastructure—cell towers to be specific) and e-commerce (industrial). These two sub-sectors of real estate rose in tandem with other growth stocks riding the AI and e-commerce megatrends but have traded lower recently as valuations have compressed. The outlook for these two sub-sectors remains promising given the outlook for continued expansion in these megatrends. Surprisingly, regional malls have been a relative outperformer year to date, despite the surge in online shopping.

Outlook

The Strategic and Tactical Asset Allocation Committee (STAAC) remains underweight in the real estate sector as commercial real estate continues to face headwinds in a post-Covid-19 world. Additionally, elevated interest rates have dampened demand for commercial real estate amid stubbornly high inflation. While yields and valuations appear attractive relative to other asset classes, bonds appear to be a safer play when considering income. The STAAC continues to recommend preferred securities within fixed income (the topic of this week's Weekly Market Commentary). Positives include an improving technical set-up for real estate, as market breadth has improved and 71% of stocks now trade above their 200-day moving average, and demand tailwinds for data centers, and potential downside for interest rates if economic growth and inflation cool.

Additional content provided by Kent Cullinane, research analyst for LPL Financial.

Jeff Buchbinder is chief equity strategist for LPL Financial.