The first quarter earnings season is largely in the books, and it was excellent. In fact, S&P 500 earnings per share (EPS) would have been up double digits in the quarter if not for a big loss Bristol Myers Squibb (BMY) absorbed in an acquisition. Even with that nearly three-point drag from the drugmaker, a nearly 7% increase in earnings—the biggest since the first quarter of 2022—is impressive. Big tech strength was again the primary driver, and estimates impressively rose.

Impressive Numbers

In our earnings preview commentary on April 8, 2024, we predicted three to four percentage points of upside to the then-consensus estimate of 3%. It turns out that estimate will be right on the money, with earnings growth tracking near 7%. That sounds good, and it is, but it could’ve easily been quite a bit better. If not for BMY, that number would be about 9.5%. Remove biotech and pharmaceuticals and S&P 500 EPS would be up 10.5%, with about 20 S&P 500 companies still left to report.

That said, all results count, as there are always big drags from somewhere. But that doesn’t change the fact that earnings are currently growing at a solid mid-to-high-single-digit pace with a realistic opportunity for even stronger growth in the coming quarters.

Margins On The Upswing And Don’t Appear Particularly Stretched

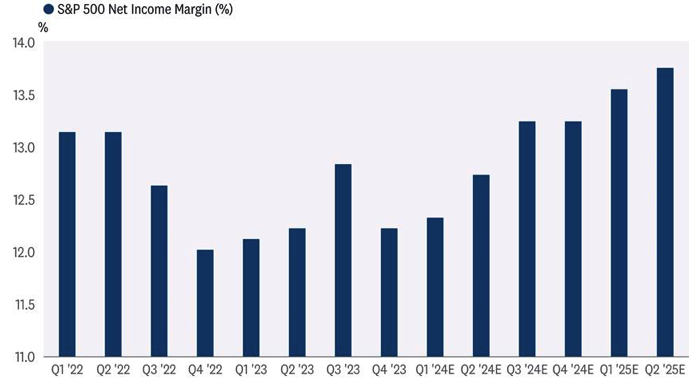

Better-than-expected profit margins played a role in the strong first quarter numbers. The S&P 500 net margin is tracking to 12.3% for the first quarter, up from 12.2% in the seasonally stronger fourth quarter. That doesn’t sound great, but given consumers are starting to push back against higher prices, a developing theme echoed by Starbucks (SBUX), McDonald’s (MCD), Target (TGT), and others, and the first quarter is seasonally weak, this is a solid result.

If companies can continue to control costs, then improving margins for the rest of the year seems doable. Economic growth is supportive. Wage pressures seem to be stabilizing as the job market loosens up a bit. Consumer prices are increasing at a faster pace than wholesale prices, using the latest readings for the Consumer Price Index (CPI) and Producer Price Index (PPI), which supports margins. And margins in healthcare and energy are depressed and poised to reverse. One risk is further consumer pushback on high prices as savings dwindle. Higher commodity and borrowing costs present other potential headwinds.

Big Tech Again Drives All The Growth

We had expected mega cap technology to again drive all the earnings growth for the S&P 500 in the first quarter, and that is exactly what happened. The biggest earnings growers, namely Alphabet (GOOG/L), Amazon (AMZN), Meta (META), Microsoft (MSFT), and NVIDIA (NVDA), drove 7.8 points of S&P 500 EPS growth in the quarter, which means the rest of the market in aggregate—call it the S&P 495—experienced a 1% year-over-year drop in earnings. Growth among the mega caps is really impressive, with earnings for NVDA surging +468%, Amazon +221%, Meta +111%, and GOOG/L a not-too-shabby +56%. Guidance was also upbeat, with particular strength in AMZN and GOOG/L, which both saw estimates rise 9–10% for 2024 and 2025. NVDA’s estimates increased 2% and 5% for this year and next.

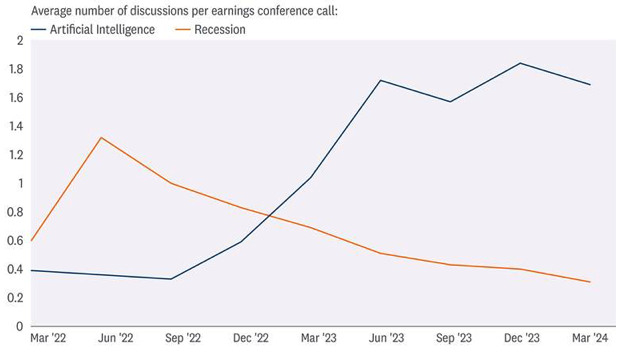

This concentration of earnings power has some investors worried. But more balanced earnings growth will likely come by the end of the year as earnings growth outside of mega cap technology accelerates, and the law of large numbers contributes to slower growth for the space. This may contribute to better performance for value stocks, but we think it’s still a bit too early to make that shift given the strength in artificial intelligence (AI). As the chart below illustrates, AI has been a hot topic on company earnings calls this quarter, and it’s not just the AI companies talking. That means more productivity is likely coming, and with it comes greater profitability for corporate America.

Our Estimates Appear Conservative

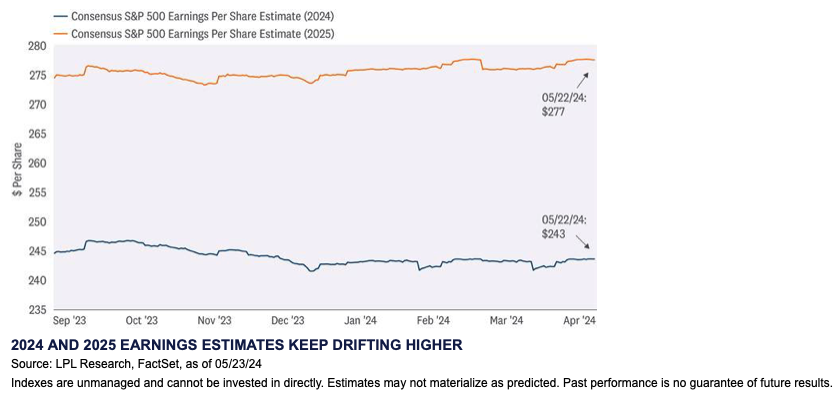

Upside to earnings estimates is par for the course, but guidance is where an earnings season can go from good to great. On that score, this earnings season was great, as estimates rose for this year and next—an unusual occurrence. Again, big tech was a big part of the story as estimates for 2024 and 2025 rose an average of 4.5% for the top five technology names. For the S&P 500 as a whole, estimates rose about 0.5%, compared with an average reduction historically near 2%.

That suggests the current consensus estimate for S&P 500 EPS near $243 for 2024 may be achievable (we will likely raise our $235 estimate in our upcoming Midyear Outlook publication). AI is providing a boost, while the U.S. economy is showing signs of picking up after the soft first quarter, and earnings declines from healthcare and natural resources may reverse. The challenge is maintaining pricing power under disinflationary conditions. And currency could potentially be a headwind if the dollar strengthens.

Looking out to 2025, slower economic growth may present a headwind. But if the AI capital investment cycle remains strong, then another year of high-single-digit earnings growth next year is quite possible. Our $250 estimate for S&P 500 EPS in 2025, much like our estimate for 2024, is probably too low, so expect that number to also be revised in Midyear Outlook 2024, due out in early July.

Conclusion

First quarter earnings season was excellent. Corporate America delivered when it needed to—when stock valuations had gotten more elevated after a strong run and weren’t getting much support from lower interest rates. Earnings growth rates were stronger than anticipated, and upbeat guidance caused analysts to increase estimates.

If companies can deliver near-consensus earnings estimates in 2024, buoyed by big tech, and inflation resumes its downward trajectory, enabling a soft landing, then we believe stocks stand a good chance of adding to year-to-date gains through year-end and hold a price-to-earnings ratio (P/E) over 20. If a slowing economy weighs on earnings in the second half and inflation remains frustratingly sticky, then we would consider fair value for the S&P 500 at year-end to be closer to our original prediction in the 4,850–4,950 range.

Jeffrey Buchbinder is chief equity strategist at LPL Financial.