Hedge funds were once the hottest investment around, but they’ve long ceded the spotlight to better performers, including private assets, real estate, technology startups and even cryptocurrencies.

The latest reminder of that is Bobby Jain’s new multi-strategy fund, Jain Global, boasting $5.3 billion in commitments and set to start trading this week. In the heyday of hedge funds, a launch of that size—one of the biggest ever—by one of the industry’s brightest lights would have been headline financial news. There’s been tepid interest.

The reason is that hedge funds don’t make money like they used to. After a blazing start in the 1990s, their performance has been on a steady decline. Hedgies have blamed numerous factors along the way, from persistently high stock valuations and aggressive short sellers to low interest rates and, most recently, a dearth of talent.

But the real culprit can be expressed in a single word: capacity. Simply put, there are only so many opportunities in markets for outsized gains, perhaps enough to successfully deploy a few tens of billions of dollars. When hundreds of billions of dollars began pouring into hedge funds in the mid-1990s, and certainly by the time they became a multitrillion-dollar business a decade later, they were doomed to disappoint.

Hedge funds have no incentive to accept that reality because it would require them to slim down, and they make a fortune on fees—on average more than 1% a year in management fees plus nearly 20% of profits. So, rather than address the core issue, they tried changing their pitch.

At the start, hedge funds claimed to be the go-to place for star stock pickers and esoteric investment strategies, such as merger arbitrage, managed futures and risk parity. But the star pickers eventually retired or ran out of luck, as almost all of them do, and once novel hedge fund strategies became mainstream and available through lower cost exchange-traded funds.

Then the pitch became superior risk-adjusted returns. Hedge funds may not be able to regularly beat the stock market, they conceded, but they’re less volatile than stocks. Wouldn’t you rather have a 7% annualized return with a 7% annualized standard deviation—a common measure of volatility where lower is better—from hedge funds than a 10% return with 15% volatility from the stock market? The answer for many investors was no.

So, hedge funds pivoted again, this time trumpeting a multi-strategy approach where they spread their bets across different assets and portfolio managers, as Jain Global will presumably do. Translation: If one high-priced hedge fund strategy is likely to disappoint, then investors should try owning more of them. It’s almost as comical as when Wall Street banks told investors in the 2000s that buying high-risk mortgage debt would magically become safer and more profitable if investors stuffed more of it into their portfolios. It didn’t work with mortgages, and it isn’t likely to work with hedge fund strategies.

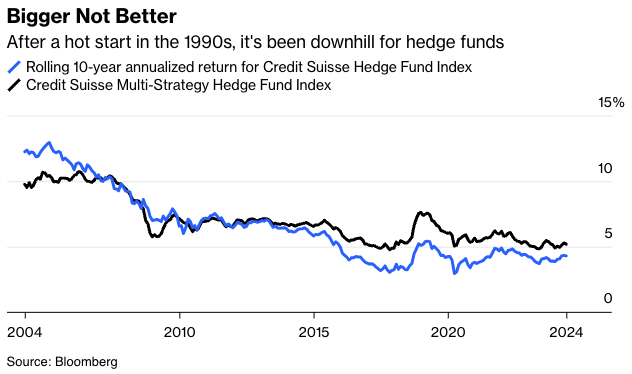

In fact, multi-strategy funds have been around for a while, and their track record is not flattering. Like the industry generally, they started strong in the 1990s and early 2000s—the Credit Suisse Multi-Strategy Hedge Fund Index peaked at 10.7% a year during the decade ending in 2004. But it’s been downhill ever since, with the index returning just 5.2% a year during the 10 years through May.

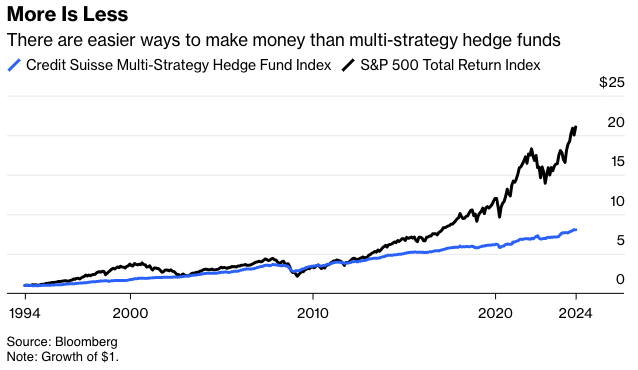

Understandably, hedge funds don’t like being compared to the S&P 500 Index because it’s a different strategy. But if the goal is to make as much money as possible, then it’s fair to ask how hedge funds compare to one of the cheapest, easiest to own and best performing investments around. And the answer is not favorably. The S&P 500 has outpaced the multi-strategy index by 3.5 percentage points a year since 1994, including dividends, and has beaten it about two-thirds of the time over rolling 10-year periods.

Multi-strategy funds say they would do better if they weren’t so shorthanded. “One of the most significant binding constraints in the industry is the availability of talent,” said Pablo Salame, Citadel’s co-CIO, in a recent interview. It’s so hard to find help these days, apparently, that Citadel had to give back $25 billion to clients since 2017 because it didn’t have enough money managers.

That’s hard to believe. Surely, Citadel could have allocated more money to the existing stable of managers. More plausibly, Citadel forfeited fees on $25 billion because it couldn’t generate outsized returns on that much money, no matter how many star managers it had.

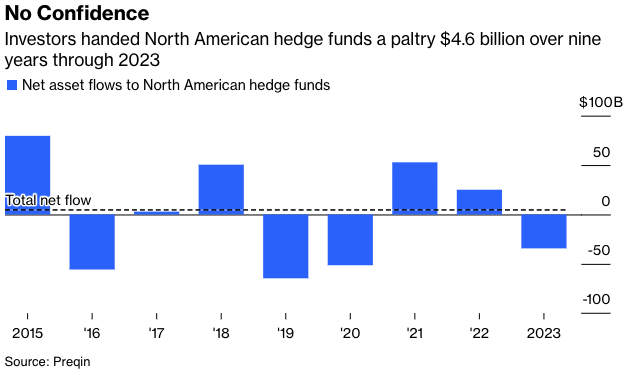

If hedge funds won’t acknowledge their capacity constraints, investors will eventually do it for them. North American hedge funds managed $3.7 trillion at the end of 2023, up from $2.2 trillion in 2014, according to data provider Preqin, but the growth in assets is largely attributable to rising asset prices. Net flows to North American hedge funds have slowed to a trickle in recent years, amounting to just $4.6 billion since 2015 through last year. Even if investors don’t yank their money out of hedge funds, the industry will lose market share as fresh capital is allocated elsewhere.

One fund understood well its capacity constraint. Renaissance Technologies’ Medallion fund is the best performing hedge fund of all time. It estimates its capacity at about $10 billion and returns money to investors regularly to keep it that size. The fund is so constrained, in fact, that there’s no room for outside investors. The funds that Renaissance does offer to outsiders are no more noteworthy than those of its competitors.

A few hedge funds may continue to make a lot of money for a fortunate few. The industry can’t do better than that at its current size, no matter how much talent it hires. The only question is how long it will take investors to come to terms with it.

Nir Kaissar is a Bloomberg Opinion columnist covering markets. He is the founder of Unison Advisors, an asset management firm.

This article was provided by Bloomberg News.